Could sustainable investing be the answer to the world's environmental problems?

Sustainable investing – the practice of incorporating environmental and social (ES) factors into investment decisions – has become increasingly popular in recent years with thousands of funds marketed as "sustainable" cropping up in the marketplace. Advocates of the practice believe it is key to lowering carbon emissions and nudging companies to adopt more environmentally friendly and pro-social behaviour, but is this how it works in reality?

A new paper on sustainable investing, which recently won the PRI Outstanding Research Award, by Professor Dirk Jenter, Department of Finance at LSE, along with colleagues Alex Edmans and Tom Gosling from London Business School, explores how sustainable funds differ from traditional funds. The researchers set out to investigate whether, why and how sustainable and other funds incorporate firms’ ES performance into investment decisions.

To find out, the researchers surveyed 509 equity portfolio managers from both traditional (290) and sustainable (219) funds. They found that asset managers across both types of fund approach investment decisions in a surprisingly similar way.

Both sustainable and traditional fund managers do acknowledge ES performance to an extent, but only insofar as it can be a predictor of long-term value and larger financial returns.

Financial returns

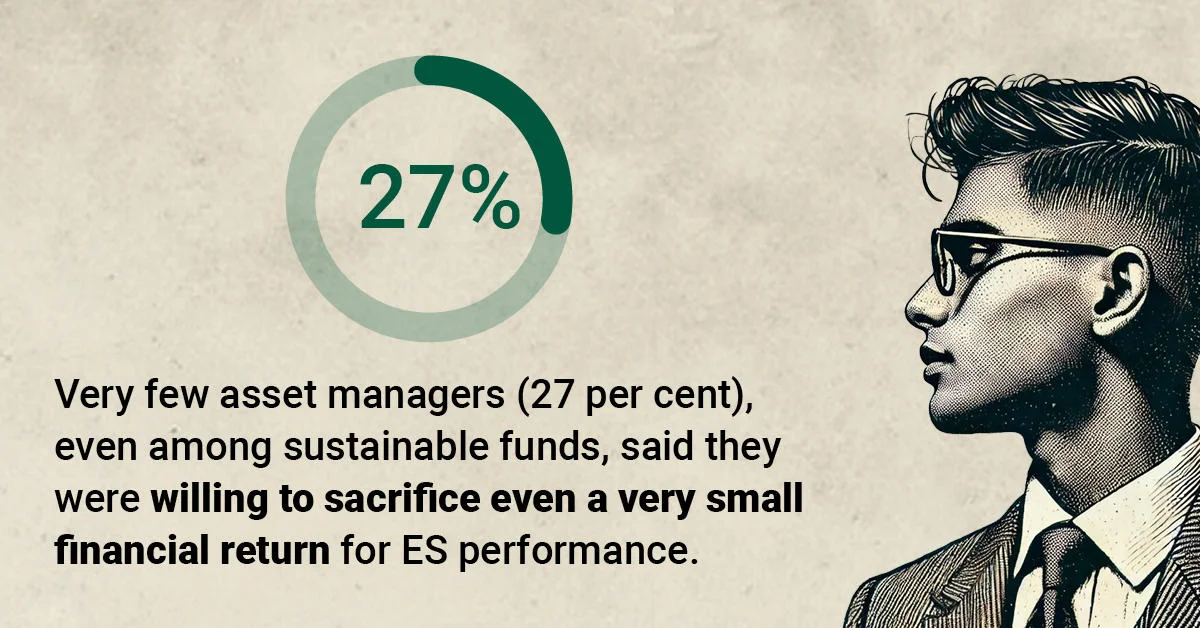

Few asset managers (27 per cent), even among sustainable funds, said they were willing to sacrifice even a very small financial return for ES performance, citing fiduciary duty – the obligation to act in the financial best interest of a client – as the reason. Indeed, one manager said: "We could never accept lower risk-adjusted returns out of the goodness of our hearts."

This finding was surprising to Professor Jenter. "I expected traditional fund managers, who don't have any sustainable labels, to tell us they were focused on maximising financial returns. But to me it was very surprising that sustainable fund managers, the ones who are explicitly marketed as responsible or sustainable, subscribed to the same goal."

When the researchers asked the asset managers to rank the importance of ES performance for long-term firm value against five other factors, both traditional and sustainable investors ranked it last, below strategy, operational performance, governance, corporate culture, and capital structure.

However, this low ranking of ES performance doesn’t necessarily mean that investors view it as irrelevant. Many free text answers given in the survey emphasised that all the factors are interlinked, and that ES can affect a firm’s competitive position. Indeed, many of the asset managers from both types of fund believe good ES performance to be a sign of a well-managed company. Sixty-seven per cent of sustainable fund managers and 61 per cent of traditional fund managers believe companies that perform poorly on environmental or social issues will also deliver negative financial returns.

One investor wrote: "it is difficult to drive long-term value if you are doing any one of these items poorly." Another added, "many of these factors are interlinked (for example, a company with good strategy, corporate culture and governance is likely to have a better approach to ES performance and capital structure)."

Thus, it appears that both sustainable and traditional fund managers do acknowledge ES performance to an extent, but only insofar as it can be a predictor of long-term value and larger financial returns.

If you’re asking [fund managers] to take environmental and social performance into account … you’re essentially giving [them] an excuse to underperform.

"Not my job"

For those hoping sustainable investing could be the answer to the world’s environmental problems, Professor Jenter believes these results show we need to be a lot more pragmatic. "I think we, as a society, need to be realistic about the fund management industry’s likely impact on how good or bad companies are. The industry won’t be leading the charge to try and make companies better, as they [asset managers] very much believe, due to fiduciary duty, it’s not their job."

If fiduciary duty is the barrier to asset managers investing more in sustainable companies, could policymakers simply relax the rules around it, creating a pot of funds with a different objective function focused less on financial returns and more on environmental and social goods?

Although Professor Jenter believes it would certainly be possible to create such a category of funds, he doesn’t necessarily believe it would be a good idea. "A fund like that would make the relationship between the client and the fund manager very tricky, as you’re giving carte blanche to fund managers to do whatever they want. If you’re asking them to take environmental and social performance into account, because these are very difficult to measure, you’re essentially giving the fund manager an excuse to underperform."

Fund constraints

Instead, Professor Jenter believes the best way forward is the use of fund constraints, which is the approach the fund industry has taken. These are essentially restrictions on the type of companies asset managers can invest in. For example, they can be constrained from investing in companies involved in arms or tobacco.

Eighty-four per cent of the sustainable fund managers surveyed said it was ES constraints, in the form of company policies, fund mandates, client wishes and reputational concerns, that have led them to make different investment decisions than they otherwise would have done, not the "sustainable" label given to the fund. These constraints can be – and often are – also used on traditional funds, resulting in even more similarities between the two fund types.

Reflecting on the findings, Professor Jenter and his colleagues believe that fund labels can be misleading and are not as clear-cut as they appear to be, with often very little difference between sustainable and traditional funds. Those who want to ensure they are truly investing in sustainable companies need to look further than the fund’s label and how it is marketed, and make sure they understand its ES constraints and scrutinise the companies being invested in.

Professor Dirk Jenter was speaking to Charlotte Kelloway, Media Relations Manager at LSE.

Download this article as a print-optimised PDF [303KB].

Subscribe to LSE Research for the World

Tom Gosling

Professor Alex Edmans

Related articles

Prioritising the climate: why international organisations are reinventing policy from the bottom-up

State effectiveness and the climate crisis

The illusion of control: why the financial sector is more vulnerable than ever to a financial crisis

Sustainability at LSE